A new overview of the MVPD market from Cowen came to two major conclusions: cord cutting is no longer the issue, and that cable-wireless convergence is “a ‘when’ not ‘if’ story.”

It’s not that cord cutting isn’t happening; it is. It’s just that cord cutting now an intrinsic characteristic of the CSP business.

The issue has become minimizing the damage from cord cutting. That means minimizing subscriber loss and protecting margins on the services that customers retain.

Cowen calculated that MVPDs will continue to lose video subscribers, mostly to streaming services (a.k.a. OTT) at a clip of about 3% year over year—at least for the near term. Satellite operators will continue to be most vulnerable to video subscriber losses.

Relief, of a sort, may be coming in the form of a new generation of consumers.

“However, our generational analysis together with our survey work shows that by 2021+, the demographic shift alone could drive a 1-2% Y/Y sub loss per annum, in perpetuity, as Generation-Z enters the workforce,” said Cowen’s new report. “Cable and Satellite, Navigating the OTT Era.”

Subscriptions from new consumers won’t compensate for subscriber losses but they will mitigate the migration to OTT.

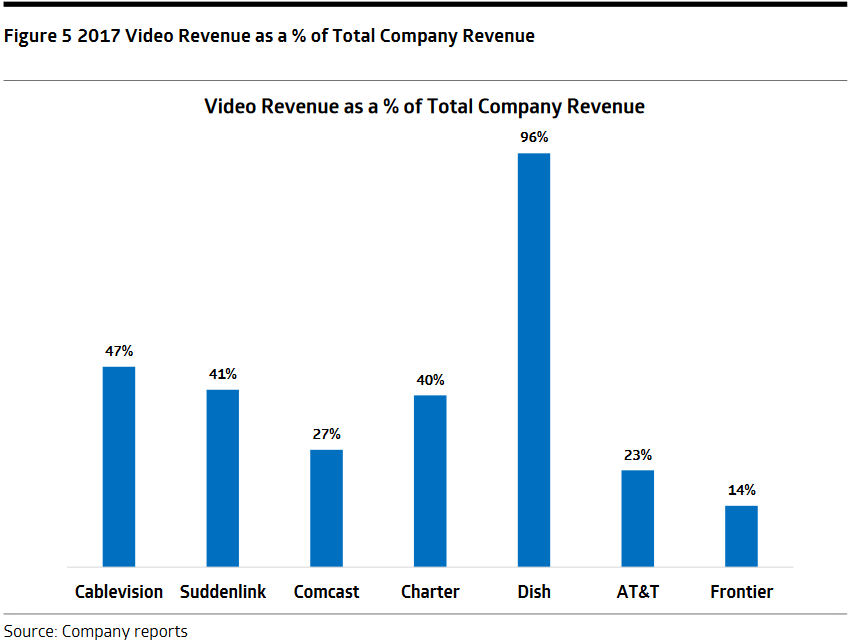

The Cowen report reiterates what cable companies have been saying all along: When they lose video accounts, those customers tend to keep their broadband subscriptions, and broadband is a higher margin product.

There has been speculation for decades that eventually MVPDs and wireless companies might converge. The expectation was that it would be cable operators who might be the first to try such a merger, so it was a mild surprise that AT&T and DirecTV were the first to combine. The other mild surprise was that nobody else has followed in the intervening years.

Cowen said it believes cable-wireless convergence is inevitable, though maybe not imminent.

Cable MSOs and wireless carriers “share the same customer base to cross-sell and up-sell,” Cowen said in the report. “Revenue synergies will therefore be meaningful. Similarly, deeper bundles reduce churn for both wireless and MSO subscribers. Lastly, MSOs will need owners’ economics (variable cost MVNO models are not sustainable in an unlimited data mobile video world), will need to participate/eliminate the 5G threat, and through wireless can enjoy lucrative new advertising data end points.”

A cable-wireless convergence doesn’t necessitate mergers, Cowen noted, “as the MSOs further develop their wireless strategies (MVNO’s, Dish NB-IoT); meanwhile wireless carriers further develop their content strategies (AT&T/Time Warner, Verizon/Oath, T-Mobile/Layer 3 TV).”

Cowen noted that MSOs are typically more patient, especially with transformative decisions. Meanwhile, the AT&T-Time Warner dispute in DOJ court has put all M&A on pause.

That said, the company believes that the “best Cable & Satellite names to play convergence are Charter and Dish.”

by Brian Santo

{kind=link}